Singapore

Singapore Hongkong

Hongkong United States

United States Group

Group Log In

Log InOn Monday, the Bank of Japan's interest rate hike set off global stock markets, and Japanese stocks fell epically, followed by a collective collapse of global markets. The strong selling pressure finally made the Bank of Japan surrender. On Wednesday, Bank of Japan Deputy Governor Shinichi Uchida publicly sent a strong dovish signal to stabilize market confidence. He said that the Bank of Japan would not raise interest rates when the market was unstable. During Uchida's speech, the yen returned to its downtrend, once breaking below the 147 mark, and the yen-dollar exchange rate fell by 2% during the day, and the Japanese stock market rebounded immediately. As of press time, Japan's Nikkei 225 index rose 2.74% and the Topix index rose 3.87%. Global carry trades will resume, the yen may be shorted again and plummet, the yen's hyperinflation will make a comeback, and the yen exchange rate will hit a new low in the near future.

Today, Shinichi Uchida's dovish remarks actually indirectly admitted that the bank's interest rate hike last week was a "catastrophic" policy mistake. UBS trader Alex Lim said in a report: "The last thing the Bank of Japan wants to see is to be regarded as the initiator of the severe market sell-off, which was in fact triggered by its July 31 rate hike." He said, "Now the Bank of Japan is clearly under pressure to respond to the market crash and may have to prove the rationality of its hawkish policy decision."

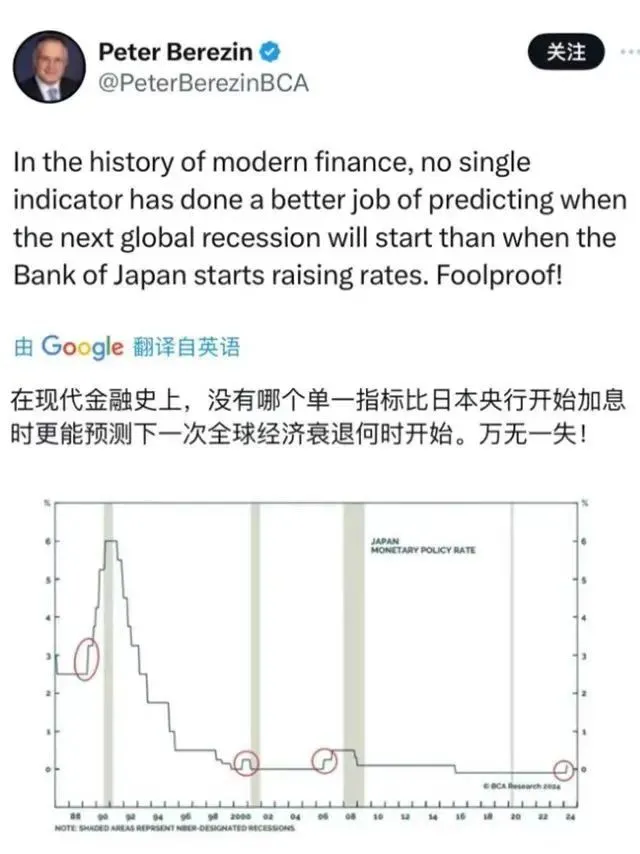

Reasons for the Bank of Japan's previous counter-trend rate hikes

In the past three decades, the Bank of Japan has always gone against the trend of Western central banks. It often raises interest rates when Western central banks cut interest rates. Interestingly, in the past 30 years, almost every time the Bank of Japan raised interest rates in the opposite direction, it was followed by a collective economic recession in Western countries, which was called the most advanced "global recession leading indicator".

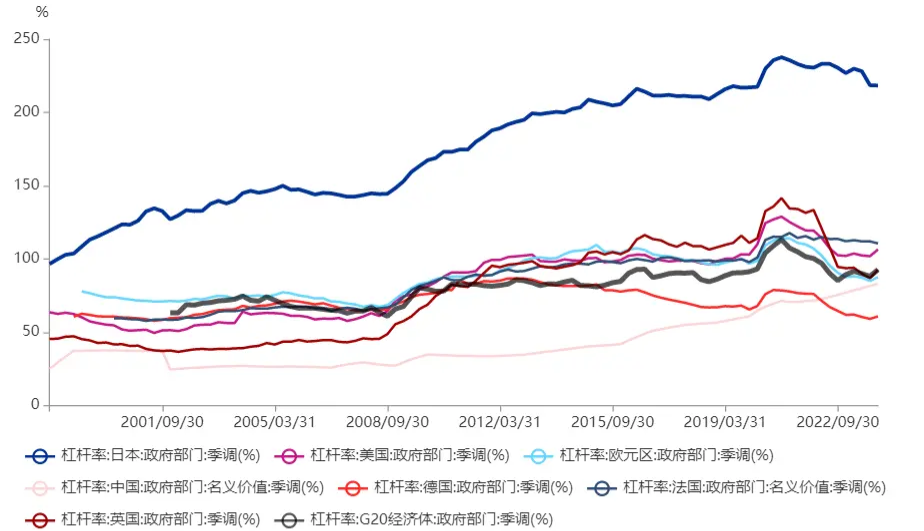

What is the reason? In fact, this is closely related to the level of Japanese government debt. As shown in the figure below, the current debt level of the Japanese government is much higher than that of other countries. As of the end of 2023, the total debt of the Japanese government will reach 129.27 trillion yen. A small increase in interest rates, even 0.1%, would increase the government's annual interest payments by 1.3 trillion yen; a 1% increase in interest rates would cause interest payments to surge to 12.9 trillion yen.

Faced with such high debt levels, the Japanese government is particularly cautious in its fiscal policy. In 2022 and 2023, when global inflationary pressures are rising, the Japanese government will maintain its quantitative and qualitative easing (QQE) and yield curve control (YCC) policies, keeping interest rates close to zero, even as other Western countries have raised interest rates. This policy choice reflects the delicate balance between the Japanese government's response to inflation and controlling debt risks.

At the end of the global economy's interest rate hike cycle and when the market generally expected interest rates to fall, the Bank of Japan took limited interest rate adjustment measures. This is not only a statement of the maintenance of the yen's currency value, but also a strategic adaptation to changes in the international economic environment. Although the Bank of Japan's action is not large, it reflects its prudent considerations between maintaining economic stability and controlling debt risks.

Will carry trades make a comeback after the Bank of Japan's dovish stance?

In the past, against the backdrop of divergent global monetary policies, the Bank of Japan adopted a different strategy from other major economies, insisting on maintaining interest rates close to the lowest levels in the world. This policy choice has led to the yen becoming a financing currency favored by international carry traders. Carry trades, which use interest rate differences between different countries to carry out capital flows to maximize profits, have become a common investment strategy in financial markets.

Taking assets in Japan and the United States as an example, over the past two years or so, the US dollar interest rate has experienced a significant increase, from near zero to 5.5% in the second half of 2023, and has remained stable at this level for a year. At the same time, the Bank of Japan's interest rate policy remains unchanged, providing favorable borrowing conditions for carry traders. It is worth noting that the famous investor Warren Buffett also took advantage of this arbitrage opportunity by borrowing yen to invest in the Japanese stock market in 2022 and 2023. Since a considerable part of the earnings of Japanese listed companies comes from overseas markets, the performance of the Japanese stock market tends to fluctuate in tandem with the US stock market.

From an exchange rate perspective, the yen-dollar exchange rate was about 115 at the beginning of 2022, and by July 2024, the ratio had fallen to around 160. This has brought significant benefits to investors who engage in carry trades. Those who invested in U.S. Treasuries not only received 10% interest income, but also received about 40% additional income from exchange rate changes. Similarly, investors who invested in large U.S. technology stocks received 30% stock appreciation based on the increase in the Nasdaq 100 Index, and the overall income was even more substantial due to the exchange rate difference. Therefore, the Bank of Japan's abandonment of interest rate hikes will make carry trades active again.

Follow us

Find us on Twitter, Instagram, YouTube, and TikTok for frequent updates on all things investing.

Have a financial topic you would like to discuss? Head over to the uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Important Notice and Disclaimer:

We have based this article on our internal research and information available to the public from sources we believe to be reliable. While we have taken all reasonable care in preparing this article, we do not represent the information contained in this article is accurate or complete and we accept no responsibility for errors of fact or for any opinion expressed in this article. Opinions, projections and estimates reflect our assessments as of the article date and are subject to change. We have no obligation to notify you or anyone of any such change. You must make your own independent judgment with respect to any matter contained in this article. Neither we or our respective directors, officers or employees will be responsible for any losses or damages which any person may suffer or incur as a result of relying upon anything stated or omitted from this article.

This document should not be construed in any jurisdiction as constituting an offer, solicitation, recommendation, inducement, endorsement, opinion, or guarantee to purchase, sell, or trade any securities, financial products, or instruments or to engage in any investment or any transaction of any kind, nor is there any intention to solicit or invite the purchase or sale of any securities.

The value of these securities and the income from them may fall or rise. Your investment is subject to investment risk, including loss of income and capital invested. Past performance figures as well as any projection or forecast used in this article is not indicative of its future performance.

This advertisement has not been reviewed by the Monetary Authority of Singapore